![]()

By Jeremy Brecher,

Senior Strategic Advisor, LNS Co-Founder

The global convergence of crises that has been dubbed the “polycrisis” has emerged in tandem with the decline of globalization. But what is replacing globalization is less a new system than a chaotic scramble. This is one of a series of Strike! Commentaries on “The Polycrisis and the Global Green New Deal.”

The introduction to my book Globalization from Below (2000) concluded, “Globalization is both irreversible and, in its present form, unsustainable. What will come after it is far from determined. It could be a war of all against all, world domination by a single superpower, a tyrannical alliance of global elites, global ecological catastrophe, or some combination thereof.”[1] It also admitted the possibility of “more hopeful” futures.

As we saw in the previous Strike! Commentary, the era of globalization is in terminal decline. We are now living in the era of “what comes after” globalization as we knew it. But what might that be?

Patterns of Turmoil

The principles and institutions that guided the world economy in the era of globalization are fading. Since the 1944 Bretton Woods agreement, long before the rise of globalization, the bedrock of world trade has been the “most favored nation” principle — agreement not to discriminate against one trade partner in favor of another. This was embodied in the Bretton Woods era through bilateral trade agreements under the General Agreement on Tariffs and Trade (GATT). In the era of globalization the principle was further enshrined in the rules of the World Trade Organization (WTO).

In the era of polycrisis, the WTO is largely ignored. Its key judicial systems have pretty much stopped functioning. The US and other countries impose tariffs – for example on imported steel – that violate the rules of the WTO with impunity. The most-favored-nation principle is now systematically violated by a plethora of “friendshoring” agreements, discriminatory governmental trade policies, and selective contracting. This represents the end of the pursuit of a “level playing field” in international trade. It is being replaced by bilateral trade agreements and invitation-only trade organizations – in effect, proto-blocs.

In the era of globalization, economic integration within nations was eroded by transnational networks that cut across national boundaries. As one team of scholars put it,

As a result of global financial integration, the transnationalisation of manufacturing activities, the increasing complexity of the international division of labor, and development at the technology and productivity frontier, the world economy has become increasingly organized as a set of highly structured networks spanning territorial borders.[2]

Although the patterns of the global economy are rapidly shifting, one thing that does not appear to be happening is a return to autonomous and internally coordinated national economies. As one indicator of this, in 2023 goods traded across borders reached their highest level ever.[3]

Rather than a return to national economies, the world economy in the post-globalization era remains composed largely of transnational networks. But these networks have been subjected to “geoeconomic fragmentation.” They are being fragmented both by negative “sticks” and by positive “carrots.”

On the negative stick side is the rapid growth of national trade restrictions. These range from export controls to investment bans. The proliferation of economic sanctions – ostensibly to protect human rights or international law but often for transparently geopolitical purposes – has greatly augmented this tendency. These interventions are redirecting the flows of goods, services, and money on the basis of government policy rather than global markets.

On the positive carrot side, “industrial policy” is providing massive public subsidies in order to redirect trade and investment to establish control over supply chains. Recent examples include

the Inflation Reduction Act in the United States, the Net Zero Industry Act in the European Union, and big investments in hydrogen and solar energy in India. The drive toward industrial policy signals “a turn away from comparative advantages and efficiencies gained from global supply chains” and a “push to control technologies’ full value chains, from research and innovation to manufacturing and deployment.”[4]

“Network Centrality”

Although the broad decline of the patterns and institutions of globalization has been widely noted, it is difficult to discern what if any structure we are transitioning to. The complex, contradictory, and at times phantasmagoric appearance of the current global economy makes it genuinely difficult to delineate. Understanding has also been obscured by the fact that so much analysis is from a partisan standpoint, proclaiming the virtue of one nation or bloc and the dastardly threat of others, rather than a single standard of judgement and attention to the interaction effects among participants. The disconnection among economics, political science, and other siloed disciplines, as well as between Marxist and non-Marxist analysis, also makes it hard to understand a polycrisis whose primary characteristic is the collision of once-distinct spheres.

A heroic attempt to portray the emerging structure of the global economy has been offered by an international, interdisciplinary outfit called the Second Cold War Observatory. Much of its work has been pulled together in a study called “The Second Cold War,” focused especially on the interaction of the US and China but along the way delineating the geopolitical and geoeconomic scene more generally. Drawing on a wide range of recent scholarship, it may be as close as we are likely to get for now to a credible portrait of the emerging character of the global economy.[5]

According to “The Second Cold War,” the breakdown of globalization is not recreating independent national economies. Rather, states and corporations are trying to establish what it calls “network centrality,” a “defining feature” of our epoch of “dense trade in parts and components, vast transnational, financial and digital flows, and networked infrastructures.”

Their definition of “network centrality” appears to be shorthand for “control over networks and their structures.” Key principles of network structure include “interconnectivity and interdependence.” As stated in the jargon of the trade, today’s geopolitical rivalry is geared towards “control over the integration of non-linear, not-necessarily-hierarchical nodes in topological networks.” However abstract the language, the reality to which it refers is more concrete. These networks are not “overtly territorial;” they have “material components” but they “transcend discrete territories.”

By achieving and leveraging network centrality – notably by controlling and connecting key nodes – actors can gain privileged access to strategic inputs, manage the circulation of information, exert control over the wider division of labor, establish standards and exclude competitors (or ensure they remain in a subordinate position), and capture value within production networks.

This competition aims to establish “centrality” in infrastructure, digital, production, and finance networks. It occurs

within the same territories, and the state or firms that establish dominance within a particular network are afforded the ability to shape inter-/intra-network integration, exclude rivals and conduct the movement of flows throughout networks. As a result, great power competition influences development trajectories, social relations, and patterns of state formation, as well as relations among state and non-state actors.

Today the great powers compete to “decouple” strategic global production networks – i.e., erect barriers in the globalized economy. This involves “relocating production to places that will allow them to exclude rivals” and “expand the influence of their domestic lead firms globally.” This can be seen today in global production networks for semiconductors, telecoms hardware, electric vehicles, artificial intelligence, and biotechnology.

These fragmented and competing networks are the prize over which rival nations and corporations are fighting.

Both Washington and Beijing leverage power in one network as they seek to gain advantages in other networks. For example, the US has scrambled to respond to the BRI [China’s “Belt and Road Initiative”] by identifying new financial modalities capable of delivering the capital for infrastructure on a comparable scale. In other words, the US seeks to undermine China’s privileged position in infrastructure networks by leveraging its power in financial networks. Similarly, China seeks to augment its formidable position within digital networks by enhancing payment systems and the digital yuan project, which serves to internationalize the RMB [Chinese currency system]. Meanwhile, Chinese SOEs [state owned enterprises] are buying into stock exchanges in Pakistan, Bangladesh and Kazakhstan, which may offer opportunities to shape global production networks.

As part of the struggle to control fragmented transnational networks, there is a growing symbiosis between national governments and their “domestic lead firms.” The corporations that have been selected to serve as protected and subsidized “national champions” are also exhibiting less and less separation from the state itself. This is particularly the case in growing military-corporate interpenetration. It is indicated not only by the expansion of industrial policy in the US and Europe, but by the recentralization of economic power in Russia and China. This does not necessarily mean that “capital accumulation” is “subordinated to national security imperatives” i.e. that the search for profit has been replaced by geopolitics. Rather, states are increasingly acting as entrepreneurs and owner of capital. The great powers consider control over strategic sectors “not only essential for national security,” but also “the basis for securing sustained long-term economic growth.” This is a tendency toward, though not yet a realization of, state capitalism.

“The Second Cold War” captures some of the principal dynamics of the world economy in the polycrisis era. Whether these dynamics will prove to be stable enough in the long run to warrant designation as “structures” only time will tell. For example, the rise of extreme nationalist and para-fascist movements might lead to (likely futile) efforts to eliminate international dependencies and restore autonomous national economies, or perhaps to adopt even more militarized solutions for national economic problems.

Such uncertainty may well be constitutive of the polycrisis era.

The Future of Fragmentation

The US by itself is unlikely to restore unipolar dominance; nor is China or Russia by itself likely to establish such hegemony. Therefore, each nation is attempting to construct alliances that will increase its capacity for regional if not global dominance. In some ways this resembles classic imperialist rivalry. But unlike most imperialist rivalry of the past, its goal is less the control of territory than the control of transnational economic networks.

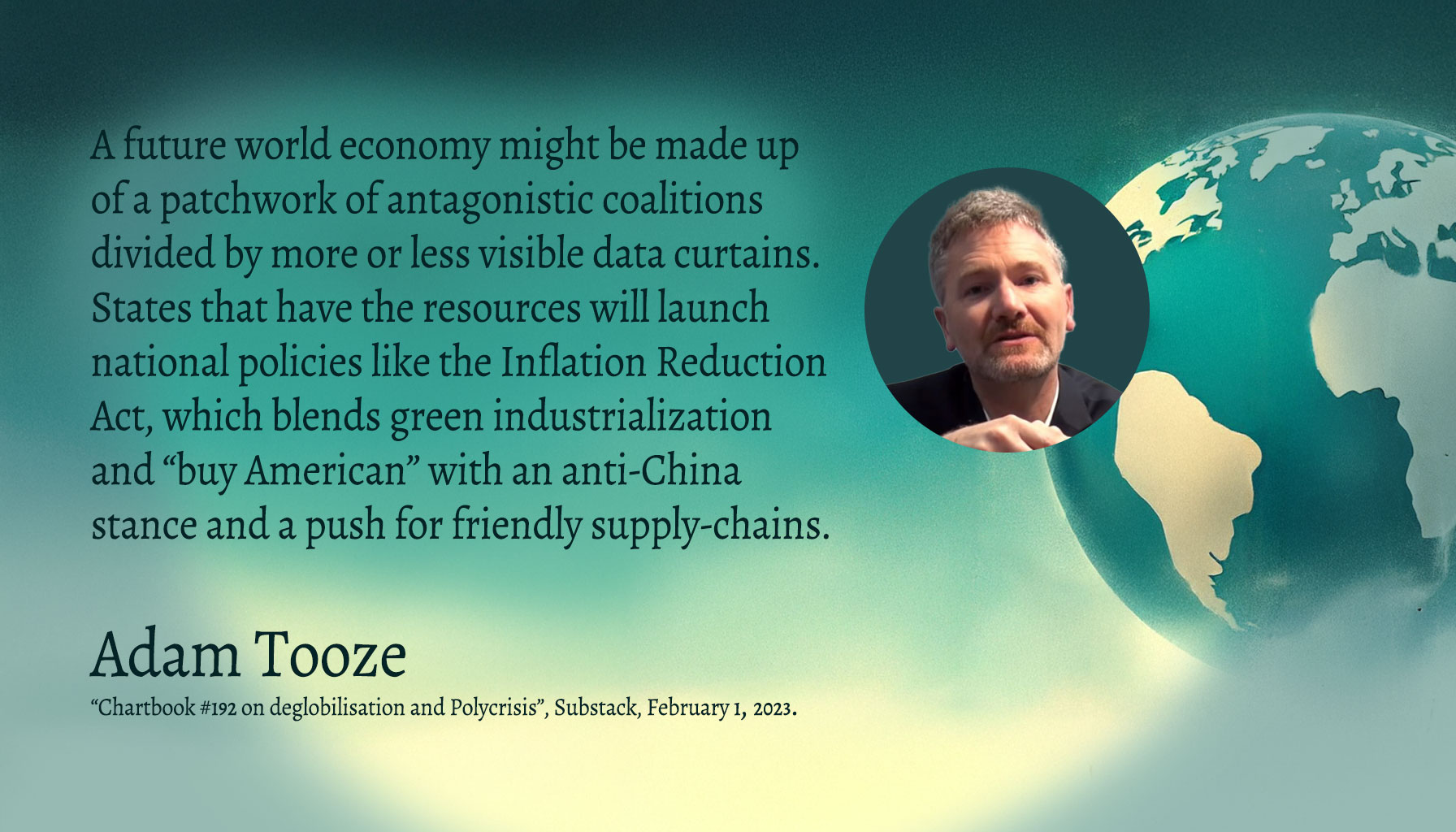

What is the future of “geoeconomic fragmentation”? At the start of 2023, economic historian Adam Tooze speculated:

A future world economy might be made up of a patchwork of antagonistic coalitions divided by more or less visible data curtains. States that have the resources will launch national policies like the Inflation Reduction Act, which blends green industrialization and “buy American” with an anti-China stance and a push for friendly supply-chains.[6]

That future sounds a lot like what is already happening. It sounds like a lot more polycrisis.

[1] Jeremy Brecher, Tim Costello, and Brendan Smith, Globalization from Below: The Power of Solidarity, Cambridge, MA, South End Press, 2002, p. xiv. https://www.jeremybrecher.org/globalization-from-below-2/

[2] Seth Schindler et. al., “The Second Cold War: US-China Competition for Centrality in Infrastructure, Digital, Production, and Finance Networks,” Taylor & Francis Online Geopolitics, Vol. 29, 2024, Issue 4, September 7, 2023. https://www.tandfonline.com/doi/full/10.1080/14650045.2023.2253432?src=

[3] Tim Sahay, “A Year in Crises,” Phenomenal World, December 21, 2023. https://www.phenomenalworld.org/analysis/a-year-in-crises/

[4] Lee Beck, David Yellen, and Noah Gordon, “How Geopolitics will shape climate action in 2024: 4 trends,” Clean Air Task Force, November 30, 2023. “https://www.catf.us/2023/11/how-geopolitics-will-shape-climate-action-in-2024-4-trends/

[5] Seth Schindler et. al., Ibid. https://www.tandfonline.com/doi/full/10.1080/14650045.2023.2253432?src=

[6] Adam Tooze, “Chartbook #192 on deglobilisation and Polycrisis”, Substack, February 1, 2023. https://adamtooze.substack.com/p/chartbook-192-on-deglobalisation